Clínica Baviera

Unknown Spanish compounder in a very attractive niche market

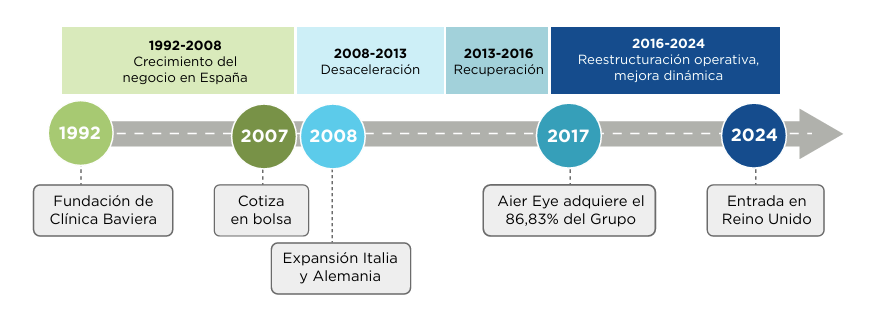

Origins

Clínica Baviera was founded in 1992. They have 33 years of experience in the ophthalmology sector, specializing in the diagnosis, treatment and follow-up of any visual disorder. The company was founded by Eduardo Baviera (still CEO of the company), Julio Baviera (Eduardo's brother and ophthalmologist by profession), Luis Raga and Fernando Llovet. The latter are also ophthalmologists by profession and together they opened the company's first clinic in Valencia in 1992.

Julio Baviera had a private clinic where he treated patients individually and was an innovator in his field because of his support for new types of surgery such as refractive surgery, whereby the patient solved his visual problems with less invasiveness. Therefore, the technology caused less impact on the client and more of the population would be willing to undergo surgery.

Going back to the history of the company, national expansion was very slow at first and then picked up pace. In fact, we could argue that the pace was too fast since CBAV made its first attempt at internationalization in 2001, when it had barely exploited its own domestic market. In fact, this attempt to expand outside Spain is a fact that shows us how real companies can fail despite being successful. They started with clinics in Milan and London. The opening of clinics is in dense populations where attracting clients to the clinics is likely. These clinics have a very high fixed cost, hence the importance of getting sufficient volume of clients. Eduardo Baviera argues that this attempt at internationalization failed because there was a lot of bad publicity in the media about refractive surgery (the operation technique used by the company) and this caused potential customers to be frightened.

The result of this experiment was to sell the London properties (Italy remained) and postpone future plans. It is important to remark that the London clinics were dedicated to aesthetic operations. CBAV had this segment until 2013. However, this failed venture was smartly done and did not result in a major setback for the company.

Clínica Baviera would try internationalization again in 2008 when it acquired clinics located in Germany and Holland. The latter were sold but CBAV kept the German ones. Eduardo Baviera was looking for acquisition targets that mainly served markets with large populations (to gain scale) and fit culturally. Eduardo would achieve his goal by buying the clinics directly from an Israeli businessman. They met in person, where Eduardo was proactive in setting up the meeting, and seeing how well they were on the same page, the agreement was reached. Since then, CBAV has gained a foothold in the German market, which is the company's second most important market. CBAV currently has operations in Italy and the United Kingdom (operations started in 2024). In both markets a seed has been planted to test if the model works and if they achieve an internationalization like the one in Germany.

A very important event is the takeover bid that CBAV had in 2017 from Aier Eye Hospital Group. This company is the largest ophthalmology group worldwide. This group bought CBAV with the aim of building a worldwide scientific group where to share the latest innovations in the sector. Eduardo Baviera was hesitant at first to take it on because of the potential cultural difference. For Eduardo, the most important thing is the people. Finally, the deal was sealed and this group is now the largest shareholder of Clinica Baviera with 89.63% of the shares. Eduardo Baviera retains 12% of the outstanding shares.

Aier Eye has subsequently reduced its ownership percentage to the current 78.23%. Combining the stakes of the relevant shareholders, the free float is only 5%. The company is working on solutions to increase liquidity without diluting existing shareholders.

This foreign ownership is a controversial issue for many investors. It is unusual to see a listed company with such a tiny free float because it has several reference shareholders. In my opinion, being part of the world's largest ophthalmology group brings more benefits than risks.

First of all, CBAV has institutional stability that allows it to focus on executing its business strategy without having potential activists pestering it. In addition, we might think that this shareholding structure also prevents a private equity takeover, which given the latent activity in the industry and the current size of CBAV could be an interesting target. On the other hand, CBAV benefits from being part of the largest ophthalmology group in the world. It has access to knowledge, networking, resources and reputation.

On the downside, there are risks that Aier Eye could decide to make a takeover bid or influence the company's strategy leading to shareholder detriment. Both of these options seem unlikely at present but are events that could come. The 5% free float does not seem to me to be a relevant risk except for high net worth individuals. One derivative of this low share availability is that CBAV may trade at lower multiples than the rest of the sector to factor in this "low liquidity risk" into the price. This seems to me to be an advantage rather than a potential risk. Low valuation + good execution is an ideal combination to holdover the company indefinitely, favoring compound interest.

Thesis

My thesis on Clinica Bavaria is that the company has a very competitive value proposition in an industry with tailwinds in its favor. The excessive use of screens will create a continuous pipeline of potential customers that CBAV will try to attract with its reputation and value proposition. The company's history is full of continuous learning (with many mistakes in between) and with Eduardo Baviera at the helm, Clínica Baviera is poised to continue to grow in this niche market.

Business model

Clínica Baviera claims to be the leading ophthalmological group in Spain in the field of laser refractive surgery. This method is the most widely used in the solution of visual problems such as myopia, hyperopia, astigmatism and presbyopia. The services offered by CBAV are pre-post operative consultations and surgical interventions. The company derives almost all of its revenue from surgical procedures to solve visual problems. CBAV opens its own clinics in Spain, Germany, Italy and the United Kingdom.

The company currently has 119 clinics distributed as follows:

81 clinics in Spain

30 in Germany

8 in Italy

18 in the United Kingdom

Spain currently accounts for 67% of revenues and this figure has remained constant over the last five years. The clinic model implemented in Spain consists of opening centrally located stores in Spanish cities with sufficient population to allow a potential density to enable rapid profitability of the clinics. Once these establishments break-even, establishments are opened in the suburbs of the cities. This model has proven to be successful as the new establishments break-even within 3 months of opening and have been able to open clinics at 7% CAGR.

In international markets the picture is different. Germany follows a similar model and path to the Spanish market (hence they share similar growth and profitability rates) but Italy and the United Kingdom are particular cases.

Starting with Italy, there is currently a change of business model from B2B to B2C. When they acquired the clinics in this country, some of them were following a B2B model based on renting the clinics to external physicians. Once acquired, CBAV management decided not to change it at first. This has caused profitability to be much lower than in the two main markets: 17% EBITDA margin in Italy vs. 30% EBITDA margin in the most relevant markets. Management is changing the business activity of these clinics to the usual B2C based on customer treatment.

Regarding the UK, this has been the last seed planted in the company's internationalization process. CBAV acquired the British company Optimax in 2024. It paid €16 million (including earn-outs) for 18 clinics. The company will apply its best practices and allocate growth capex to this geography. This segment is currently loss-making, but management expects to make these clinics profitable from 2027 onwards.

Management's objective is to accelerate the growth of opening new clinics and reach 180 clinics by 2027. From the current 137, this target would represent a 10% CAGR growth. All these openings will be carried out with 70-80 million euros of capex accumulated over 3 years and without using debt.

Clínica Baviera has been very well managed by Eduardo Baviera. Eduardo is a reflective person who seeks continuous improvement. In his book "Ideas that work" Eduardo discusses organizational and cultural aspects that have improved the company:

The R&D department is constantly reviewing what innovations are occurring in the industry and how they affect the customer. As a company policy, CBAV will not be the first company to apply new technologies but will scale that with scientific backing that improves the quality and/or safety of customer service.

Use of reasonable debt. Eduardo defines reasonable debt as that which helps the company but does not compromise its survival. He tells how in the 2008 crisis many stakeholders tried to convince him to take on a lot of debt, as it was the fashionable thing to do, but he always opposed it. In the end, Eduardo is a founder and treats Clinica Baviera as if it were another son.

Obsession with competition. CBAV constantly analyzes what is happening in the industry. This allows them to incorporate those innovations and/or changes quickly.

During the 2008 crisis, some of the measures they took to mitigate the effects were: reducing the salaries of top management, freezing the salaries of intermediate levels, containing and reducing costs and not giving dividends.

Lowering prices to take care of the most important stakeholder: the customer. According to Eduardo, the customer is unpredictable and capricious. Therefore, your service must be good, beautiful and cheap so that they continue to choose you in the long term. In the event of a future crisis, we can assume that Clínica Baviera will continue to invest in improving its services (such as the technology used) and will make moves such as lowering prices to improve goodwill with its clients. These types of actions strengthen long-term relationships. Finally, during the recent covid crisis, they decided not to raise prices even though annualized inflation in Spain was 10% in order to continue taking care of the customer.

Finally, on the company's performance in periods of stress, in the 2008-2009 period, net profits fell from 11.8 million euros in 2007 to 8 million euros in 2008. This 40% drop was due to the intrinsic operating leverage of the business against CBAV and management's decision not to increase prices and to take care of the customer. Nevertheless, CBAV was not in real danger at any time because Eduardo Bavaria is totally averse to having a lot of debt. The company's balance sheet was healthy and cash generation was able to sustain complex periods. Even so, in the event of going through a similar period again, we could encounter an opportunity cost risk.

On the other hand, I think that CBAV has improved structurally since then due to: 1) the sale of a former aesthetic operations division that was a much worse business than ophthalmological operations and 2) the crisis caught the company in the middle of internationalization. Today the company is in a better position to face a similar situation.

Tailwinds

In Spain, 8 out of 10 Spaniards have a visual problem. This means approximately 39 million people could be potential customers for CBAV. According to the study of vision in Spain (2022 version) 39% of Spaniards have myopia. In addition, the incidence of myopia has increased by 10% among 18-24 year olds. CBAV has tailwinds in this field due to the fact that practically all of the new generations live glued to a screen. These screens are generally located at a short distance from our eyes, so there is a greater overexertion in having to focus on a nearby object.

Despite the fact that 80% of the population has some visual defect, only 13% have had surgery. Progressively we can expect greater penetration due to technological progress that is less and less invasive for the client. The company itself estimated in 2019 that the penetration of eye surgery in Spain was 8-9% (one of the highest worldwide) while in Germany or Italy this figure was 2-3%.

It is striking to note that 72% of those interviewed state that they underwent surgery to improve their quality of life. If we include in the above figure those who underwent surgery to improve their health, this brings the number to 87% of those operated on. In my opinion, with the current trends of looking better for oneself and putting more resources into health, this seems to me to be very positive for the long-term impact of the company.

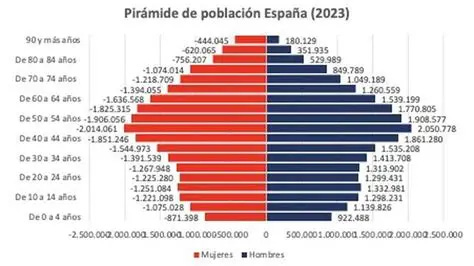

This, in conjunction with the reverse population pyramid where both Spain and Germany, 20% of the population is over 67 years old, should be important drivers of demand for Clínica Baviera.

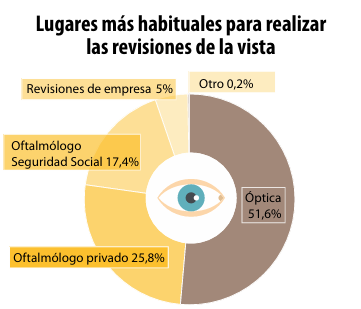

In addition, 52% of those interviewed say that they have their eye examinations at an optician's, while 26% do so at private ophthalmologists. I find this breakdown interesting since the weight of private clinics such as CBAV is greater than social security (public healthcare in Spain), which shows that the value proposition is perceived by customers. They are paying for a service they could get for free. This is mainly due to the lack of capacity of the public service to offer specialized medical consultations quickly. Regarding opticians, Eduardo Baviera defines them as indirect competitors. They provide a substitute product (you can fix your myopia by wearing glasses instead of having an operation) but they attack different solutions for the same problem.

Opticians will continue to be a relevant part of the industry because not everyone is open to having surgery. However, in my opinion, what is relevant here is to observe how governments (especially the Spanish one) are unable to provide a complete welfare state. Their excessive indebtedness (and therefore their lack of capacity to invest in healthcare) and the trend of an aging population mean that public healthcare systems are increasingly deficient, giving traffic to private ophthalmology clinics.

Finally, the market is expected to be €31B in size by 2028. This implies a growth of 5% CAGR. The competitive landscape is highly fragmented. According to Lincoln International, approximately 70% of ophthalmology treatments are performed by small independent clinics. Competition is therefore highly dispersed and CBAV's ability to provide a higher value-added service is critical to continue to gain market share. As in much of the industry today, consolidation looks set to occur gradually. Those with scale will be able to afford to invest more in providing better service, raising awareness and investing in new technology and equipment.

Financial statements

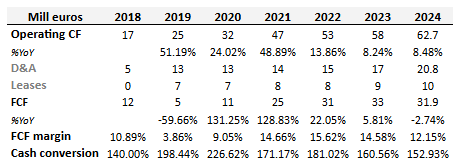

Financially, the overall development of the company has been magnificent. Eduardo and his team are executing perfectly. They have managed to grow revenues at 23% CAGR since 2018. Management has increased prices at 2% CAGR while the rest has been volume driven. This pace of sales has occurred at the same time that both EBITDA margin and operating margin have increased substantially. The intrinsic operating leverage of this business has played a fundamental role in the expansion of margins.

Around 65% of the EBITDA generated comes from the Spanish market. Germany accounts for 22%. Italy generates around 4% and the United Kingdom do not currently contribute. However, any improvement in both markets would be a very positive optionality for the company.

If we analyze the development of EBITDA per clinic, we observe that each Spanish clinic generates 700K euros in EBITDA. The figure for the German market is 500K euros EBITDA/clinic and 400K EBITDA/clinic in Italy.

The expansion of clinics has been financed through its operating cash flow, with no use of debt or equity issuance. Its financial position is net cash from 2020. This reflects Eduardo Bavaria's adversity to having more debt than is reasonable and the ability of the core business to generate cash.

With respect to significant capital allocation items, Clínica Baviera operates a business where capex represents (on average) 10% of sales. Of this capex, approximately 50% is maintenance.

While CBAV has to spend on capex to continue its business (opening and improving facilities), working capital is negative. This is because most treatments are paid for the same day they are performed. This allows CBAV to have more resources to reinvest. Considering that ROIC is 37% and ROIIC is 30%, every euro allocated to reinvestment generates tremendous value.

In the 2018-2024 period, Clínica Baviera has reinvested, on average, 60% of its operating cash flow in capex, leases and m&a. It is relevant to include leasing expenses in the financial metrics calculations because CBAV leases part of its clinics. I consider these expenses as a type of capex. Reinvestment may seem low but it is important to emphasize that 30% of the operating cash flow goes to dividends.

The 60% that is reinvested is at very high rates. The ROIIC for the last 7 years is 33%, 60% for the last 5 years and 31% for the last 3 years. If you multiply the reinvestment rate by the ROIIC, I get that CBAV has grown at 18% CAGR its intrinsic value.

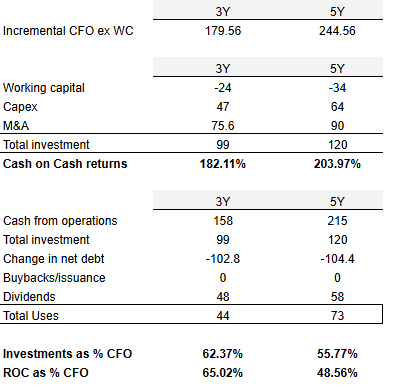

The following analysis I have copied from @bizalmanac (follow him on X) and it is a very good method to analyze the cash returns obtained by the company. Here we see that CBAV gets extraordinary results. In periods with lower demand we could see a reversal of working capital. In this case, we would see a decrease in cash returns. Still, these are extraordinary results that show us the profitability of the underlying business.

If we look at classic returns on equity, the results are equally very positive. CBAV's floor has been at 20% with its ceiling in 2021 with returns of +40% on capital employed. As the recent open clinics mature we can expect this trend to continue. In the more bearish case we might think that if the company reaches maturity in opening clinics, these returns will decline to the organic return of the business without the inorganic contribution. This is an aspect to monitor but management rules out that they will not be able to continue opening stores at the current rate for the foreseeable future.

Board of Directors

The key management person is Eduardo Baviera. He has been the CEO of Clínica Baviera since its foundation. He has a relevant stake in the company (12%). In addition, he receives 273K euros in fixed salary, 109K euros in variable remuneration and 12K euros in other items. Eduardo is a manager with soul in the game and his involvement is beyond any doubt. For shareholders, the positive thing is that he will remain with the company in the medium to long term.

The rest of the board of directors is made up of 7 people. The total remuneration to this group of people is €1.7M (2% OCF 2024). I have not been able to find information on how long they have been with the company but based on Eduardo Baviera's book, it would appear that most of the company's executives are internal hires. Eduardo values demonstrated skills more than people's resumes. This is a positive sign that reinforces CBAV's corporate culture.

The company's remuneration policy is based on:

Fixed remuneration. The amount will be associated with the position and experience but can never exceed 400K euros.

Variable remuneration. This remuneration is related to certain parameters:

Financial performance criteria: net profit, EBITDA, cash flow, investments and compliance with the development plan, performance compared to other securities and shareholder remuneration indexes and financial strength.

Non-financial performance and sustainability criteria: safety levels, quality of medical service, key personnel turnover ratio and compliance with objectives.

The objective of these criteria is to ensure the sustainable development (without using too much debt) of the company and labor stability. Variable compensation is paid in cash and may never exceed 200% of fixed compensation. There is currently no compensation based on SBCs. Finally, the company's key personnel have non-compete agreements for 2 years following their departure from the company. The incentives in place and this clause should discourage key personnel from leaving the company to direct competitors.

Finally, Aier Eye Hospital Group has 4 directors in CBAV. These advisors do not exert any pressure on the company's strategic decision making, but rather support what Eduardo and the rest of his team think. The advisors have an oversight and monitoring role. All of these people have extensive experience in the sector with relevant positions within Aier Eye.

Competitive advantages and risks

Advantages:

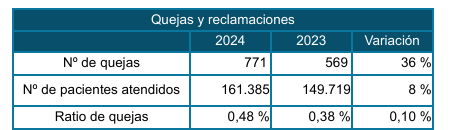

Reputation. Going blind is a problem that nobody wants to have, so you will choose the company with the best reputation in case you want to have eye surgery. Here CBAV stands out due to its scale, well-known brand and decades-long track record. Its negligible number of complaints demonstrates the quality of the service provided to the client.

% of Complains per year

Scale. Operating leverage in this industry is very important due to the high fixed costs of operating clinics. CBAV through its scale manages to take advantage of this. If a competitor wanted to imitate the company it would first have to invest in the development of a clinic. Subsequently attract sufficient volume to be profitable. However, without a prior reputation, it is complex to attract volume that trusts you in something as precious as eyesight. Also, aspects such as hiring quality staff and expertise in technical knowledge make it difficult to attract new competition.

Network effect. Word-of-mouth marketing is the fundamental marketing of the company where satisfied customers are the ones who communicate the benefits of the business. This causes a greater number of people to come to Clínica Baviera for their operations. Moreover, in case you have already undergone a treatment with the company, it loses sense to switch you to another clinic as CBAV has all the information about your case.

Risks:

Dependence on qualified personnel. In case of losing highly qualified personnel, especially health personnel, the company could be negatively affected. CBAV tries to integrate and retain its staff through intensive training where new employees learn all the necessary technical knowledge. During this process, which lasts for months, the rookies get to know each other and form strong bonds.

Demand cooling. CBAV has grown its revenues due to higher trading volume rather than price increases. The risk of lower demand is applicable to all companies but it seems to me that in this case it is an important risk to consider. These are discretionary operations (65-70% of interventions are for convenience) that in many cases could be postponed. This risk has already materialized during the great financial crisis and the European bond crisis.

Exit of Eduardo Baviera. The Baviera brothers founded the company and Eduardo has been the CEO since its inception. This is a common risk in companies with founders at the helm, but the transition at CBAV can be complex. Fortunately, Eduardo looks set to remain at the helm for the next few years but it is a risk to be taken into account in the medium term.

Acquisition. I have read several articles highlighting an increase in the number of private equity buyouts in this sector. Due to the size of CBAV, its operational excellence and valuation, it may be the target of a similar operation. On the other hand, the Chinese majority shareholder could also be a source of a takeover bid. A priori, this risk is currently not significant as the group does not actively intervene in CBAV's decisions.

Valuation

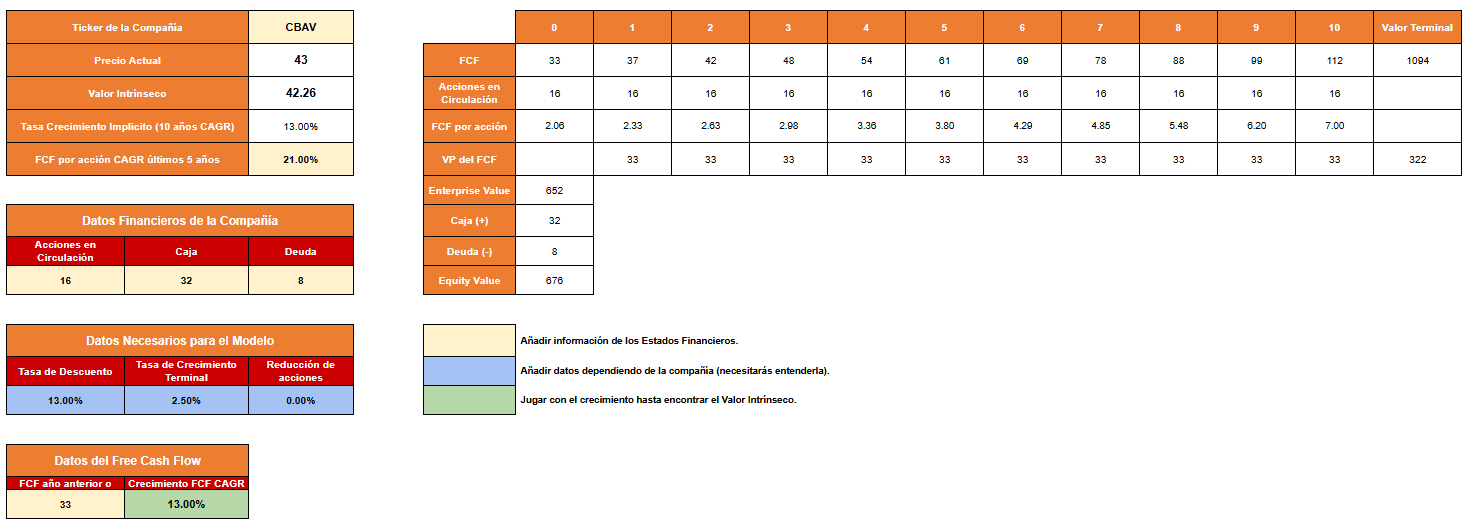

Reverse cash flow discount

Clínica Baviera is currently trading (July 5, 2025) at 43 euros per share. In my model I introduced the following subjective inputs:

Discount rate: 13%. The discount rate is higher than usual due to the fact that the company may suffer in periods of economic crisis. It is not a thesis-breaking aspect but it does make me demand a higher return for investing in it.

Terminal growth rate: 2.5%. It is a business that will eventually reach maturity and with this terminal growth reflects that aspect.

Share reduction: no impact. The free float is very low, so I rule out any significant buyback program. In case of a very attractive M&A opportunity, shareholders could be diluted but, seeing the modus operandi of small bets in the internationalization period, I see this as unlikely.

With all this plus the 2024 financials, CBAV should grow its FCF at 13% CAGR to get 13% IRR on the company. This growth, compared to that achieved over the last 7 years, seems affordable. My average price is around €32 per share, which would imply a 9% FCF CAGR to obtain the same IRR. After the company's share price rally, the valuation is tighter but not too demanding.

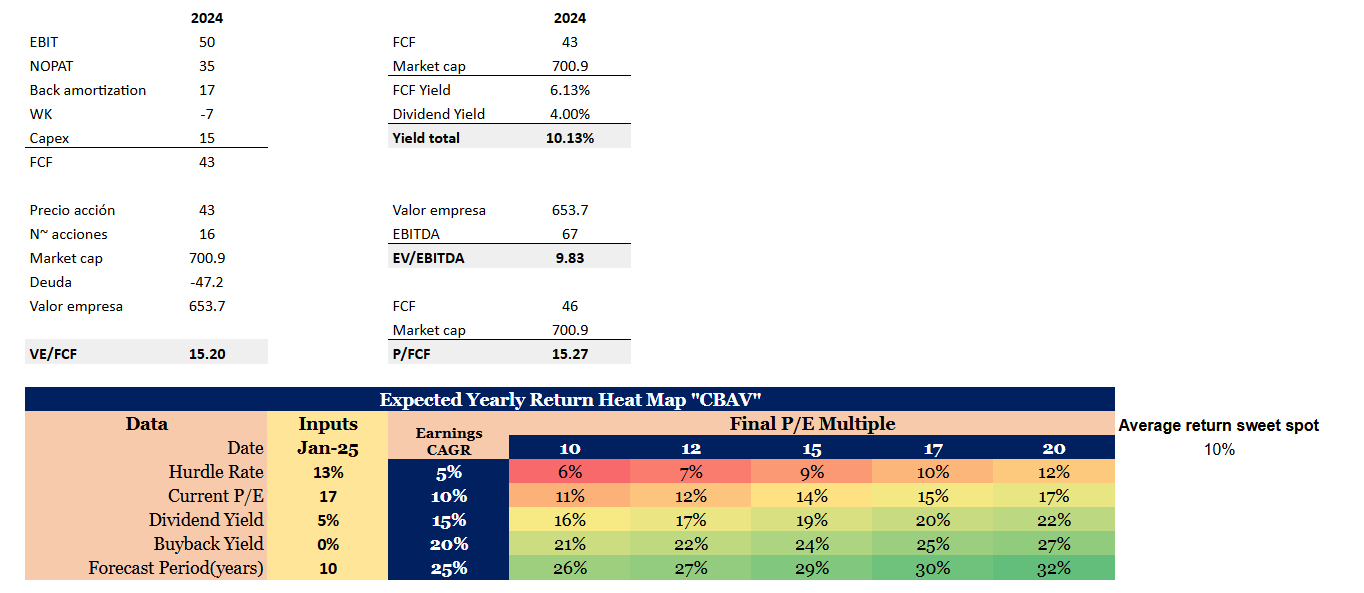

Valuation multiples

CBAV's yield is currently 10%. Considering the current situation with very demanding market valuations, this seems to me to be an attractive starting valuation. In the model below, looking at the earnings growth variables and the exit multiple, my conservative combination is 5-10% revenue growth and an exit multiple of 10-15x, the average return is 10%. It doesn't look like a very attractive return but the current FCF is far from mature FCF. Once the clinics mature we will see the true earnings power of the company. In any case, a 10-15% drop in the share price would put us at an expected return of 11-12%. Since I bought CBAV, the company has become more expensive but there is still room for good returns.

Conclusion

Clínica Baviera seems to me to be one of the few stories of a quality company in my home country (Spain) with a manager in charge who has built the company from the ground up.

Eduardo Baviera's execution has been superb and with mistakes in between, CBAV is in an ideal situation to benefit from the tailwinds of its sector. After reading his book, "Ideas that Work," the company's culture is focused on constant learning and innovation. In an industry where learning and adoption of technologies and methods is vital, it seems to me that this is the right culture. In short, it is a company run in a humble and honest way, whose units economics are superb and with the current tailwinds I expect it to grow its operating cash flow in double digits throughout the economic cycle.

Disclaimer

This article is not and does not intend to be a recommendation to buy and/or sell. Each person should do their own research before making an investment decision.

Great analysis, I don't understand your total yield metric however. Adding up dividend yield and FCF yield is double counting. After all dividends are paid out of the FCF produced.

Clinica Baviera moved to my watchlist, sadly I haven't noticed this one a few years ago! Too expensive now for me.

Do you have any guidance for FY 2025 or 2026?