Tonnellerie Francois-Frere

Empresa familiar centenaria en un sector aburrido pero lucrativo.

Introducción

En el entorno actual hay una gran base de inversores que se sienten mayoritariamente atraídos por inversiones exóticas, ya sean en sectores de moda ó geografías remotas. Sin embargo, hay empresas e industrias que pasan por debajo del radar. Estas compañías, de forma general, abarcan nichos de mercados que no se comentan pero que son muy lucrativos. En la tesis de hoy, hablaremos sobre una empresa que primordialmente fabrica y vende barricas de madera. Puede sonar a una inversión poco excitante, sin embargo, detrás se esconde una empresa familiar centenaria que ha creado mucha riqueza.

Tras un periodo amplio donde la acción no ha hecho nada, vamos a detallar cómo ha evolucionado el negocio y determinar si puede haber una oportunidad de inversión.

Historia

Esta empresa tiene sus raíces en la tonelería François Frères, fundada en 1910 por Joseph François, el bisabuelo de Jerome François, actual CEO. A lo largo de los años, la empresa ha experimentado varias generaciones de liderazgo y expansión internacional:

1910: Joseph François funda la tonelería en Saint-Romain.

1917: La segunda generación, Robert y Henri François, continúa con la tradición de su padre y establece la empresa François Frères Cooperage en 1942.

1959: La tercera generación entra en escena con la llegada de Jean François, quien fortalece la relación especial con los productores franceses, especialmente los de Borgoña.

1972: Jean François y su esposa Noëlle François asumen la dirección diaria de la tonelería y expanden las ventas internacionales. Los primeros barriles de François Frères aparecen en Italia y llegan a las bodegas de Robert Mondavi en California.

1980: La tonelería se moderniza y se instala en las afueras de Saint-Romain.

1982: François Frères gana el “Grand Prix de l’Exportation Artisanale”. La expansión internacional continúa con pedidos de barricas para Rosemount Estate en Australia y la importación de barriles a Argentina por parte de la familia Catena.

1989: Jérôme François, hijo de Jean y Noëlle, se une a la empresa como la cuarta generación, contribuyendo a la diversificación y expansión internacional del Grupo TFF.

1995: La tonelería adquiere “Tronçais Bois Merrain” en Allier y luego SO.GI.BOIS, el principal productor de duelas en Francia.

2002: Se crea Joseph François para producir una amplia gama de recipientes de madera.

2010: François Frères Cooperage celebra un siglo de experiencia y excelencia al servicio de los grandes vinos.

Modelo de negocio

Tonnellerie Francois Frere es una empresa familiar francesa, actualmente dirigida por la cuarta generación de la familia Francois, dedicada principalmente a la venta de barricas de roble para los sectores del vino, el whisky y el bourbon.

Las barricas de roble forman una parte esencial de la cadena de producción de las bebidas alcohólicas. Gran parte de la calidad de las bebidas alcohólicas viene determinada por cómo y cuanto tiempo se ha madurado el producto. Por ejemplo, a igualdad de condiciones, un vino madurado 30 años será de mejor calidad que un vino madurado por 2 años. El principal incentivo para esperar 30 años a vender tu producto (y los costes que hay que incurrir para ello) es la posibilidad de poder vender el producto a un precio elevado. El caso más extremo de esto es que el vino más caro del mundo, una botella Romanée Conti madurada desde 1945, fue vendida por 558.000 dólares en 2018.

Esta opcionalidad de disfrutar de precios de ventas mayores provoca que haya empresas que estén interesadas en madurar su producto por mucho tiempo. ¿Cómo lo maduran? Principalmente en barricas de roble.

Las barricas son las responsables de aportar los aromas y los sabores de las bebidas. De hecho, dependiendo del tipo de roble que se use, las connotaciones de aroma y sabor serán diferentes.

Roble americano. Es una madera dura, resistente y permeable. Aporta aromas más dulces, a la par de fuertes. Ejemplos: aromas a café, cacao y coco.

Roble francés. Es una madera más blanca que se caracteriza por aportar aromas más equilibrados, como balsámicos, miel o frutos secos.

Roble español. No se utiliza tanto para el vino. Sin embargo, su capacidad aromática es mayor.

La elección del proveedor (TFF en este caso) y del material a emplear para la barrica es importantísimo. La empresa cuenta con un mejor producto en un sector donde el valor añadido es muy importante:

Selección de Madera: Utilizan madera de roble de alta calidad, principalmente de los bosques franceses de Allier, Tronçais, Vosges y Nevers. Cada bosque aporta diferentes perfiles de sabor y aromas.

Tostado Personalizado: François Frères ofrece una variedad de niveles de tostado, desde ligero hasta fuerte. Esto afecta la liberación de compuestos aromáticos y la estructura del vino.

Grano Fino: La madera de grano fino utilizada en sus barriles permite una integración suave con el vino, sin dominar los sabores.

Artesanía: Los barriles se fabrican con precisión artesanal, asegurando uniones herméticas y una forma perfecta.

Capacidad y Forma: Ofrecen diferentes tamaños y formas, como barriles de 225 litros (formato estándar para el envejecimiento de vinos tintos) y barriles más pequeños para vinos blancos y licores.

Innovación: François Frères ha desarrollado tecnologías como el “Barril de Precisión” para un control aún más preciso de la tostado y la permeabilidad.

TFF ha sido históricamente el jugador más grande a nivel mundial en la producción de barricas. Han integrado verticalmente todo el proceso, desde la obtención de la madera (el 90% de la madera que utilizan es suya) hasta la fabricación de las barricas y sus múltiples detalles. Esta integración vertical ha permitido a la empresa ganar un know how, una escala y una reputación que no es replicable.

El crecimiento de las ventas de TFF Group ha venido determinado por un mix de crecimiento orgánico e inorgánico. En su objetivo de integrar verticalmente todo el proceso productivo y expandirse horizontalmente a otras bebidas alcohólicas, la empresa adquiere otras compañías de menor tamaño, generalmente aserraderos, cooperativas..que le permite seguir ganando escala y know how.

Sin embargo, también han sucedidos adquisiciones no relacionadas con las actividades principales. Por ejemplo, han adquirido tres empresas de productos de madera para enología y una empresa de barricas de acero inoxidable. El motivo de estas operaciones es reducir el riesgo de disrupción del negocio principal, extendiendo sus actividades a nuevas partes del sector. Los productos de madera para enología hace referencia a introducir partes de madera en las bebidas alcohólicas para otorgar matices de sabor y aroma. Digamos que es un método low cost de poder mejorar tu producto. En lugar de depositar tu bebida en un barril, depositas la madera en tu bebida. Por último, los barriles de acero inoxidable es un método moderno para almacenar bebidas alcohólicas, en especial el vino. A priori, esta diversificación está teniendo éxito. En el último año, estas actividades representaron un 20% de los ingresos del sector del vino.

Respecto a los sectores que abarcan, históricamente la empresa ha estado exclusivamente dedicada al sector del vino. Sin embargo, a finales de la década del 2000, se introdujeron en el sector del whisky escocés. Los motivos que les llevo a esta expansión fueron 1) Apenas hay crecimiento en el sector del vino y 2) auge del sector del whisky escocés. Es relevante destacar la importancia de que el whisky sea escocés. En las bebidas alcohólicas, hay ciertos productos que disfrutan de monopolio geográfico, es decir, solamente se pueden producir estas bebidas en una sola región. El whisky escocés solamente puede ser fabricado en Escocia, el bourbon es la bebida nacional de los EE.UU y solamente se puede producir en Kentucky, los vinos Rioja en la zona de la Rioja (España)…Esto provoca que haya grandes ventajas para la primera empresa que se adentre en este mercado y consiga un tamaño relevante dentro del sector.

Debido a estas características, TFF Group ha ido adquiriendo cooperativas y fábricas en Escocia, con el objetivo de conseguir una posición relevante dentro de este sector. Y de hecho, lo han conseguido. La empresa aclama ser la cooperativa independiente número 1 globalmente. Todo ello en un periodo de 15 años. Esta expansión a nuevas bebidas le permite disfrutar de un crecimiento sostenido y mayor diversificación.

En 2015 iniciaron una nueva expansión, en este caso al sector del bourbon. En su informe anual destacaron los siguientes motivos para adentrarse en este sector:

Mercado donde la producción está altamente regulada y la denominación de origen bastante protegida.

Mercado bastante dinámico, con crecimiento en los años venideros.

Para poder introducirte en este sector, al ser una bebida con regulación de denominación de origen, las empresas tienen que comprar activos en la zona de Kentucky, donde se produce el 95% del bourbon. El bourbon es la bebida alcohólica nacional de los Estados Unidos.

Además, existe venta cruzada entre el sector del bourbon y el sector del whisky. Las barricas de roble americano utilizadas para madurar el whisky han sido usadas previamentes en la maduración del bourbon. Está actividad se realiza debido a las connotaciones de aroma y sabor que el bourbon desprende, que posteriormente se incorpora al whisky. La oferta y demanda de barriles para el whisky puede sufrir grandes oscilaciones, debido a la falta de oferta (depedencias del bourbon) y del aumento de los precios de la madera. Sin embargo, la subida de precios compensan el menor volumen de barriles. Por último, TFF Group también dispone de una división de reparación y mantenimiento de barriles, que suele tener crecimientos explosivos en periodos de falta de nueva oferta (+34% crecimiento en 2023).

En el periodo de 9 años, el bourbon ha pasado de ser la novedad de la empresa a representar el 37% de las ventas en 2023. Sin duda, la directiva tiene un gran conocimiento de todo el sector de las bebidas alcohólicas.La experiencia y la cantidad de datos que pueden llegar a manejar provoca que se puedan adelantar a futuras tendencias del sector y, al ser el primer jugador en mover ficha (y tener mayor cantidad de recursos), se pueden llegar a convertir en jugadores dominantes de nuevos sectores. Esto jugó un papel importante en la decisión de expandirse al sector del bourbon. Además, la rentabilidad del segmento está aumentando gracias a la integración de las adquisiciones y la maduración de las inversiones realizadas en capex. Actualmente el margen EBITDA del bourbon es del 17%, superando el margen objetivo que estableció la directiva del 15%. Por último, se espera que el crecimiento del sector continúe, teniendo en cuenta las inversiones que están realizando las siguientes empresas:

Esta expansión al bourbon ha provocado un cambio en el mix de ventas por segmentos y países. Históricamente, el segmento del vino ha representado casi la totalidad de los ingresos de la compañía. Esta dependencia fue disminuyendo hasta que, el año pasado, por primera vez, el segmento de licores, en su conjunto, representó más de la mitad de las ventas de TFF Group. Respecto al mix por mercado, la transición a los licores ha provocado que el principal mercado que atiende TFF sea Estados Unidos, el cual representa un 55% de las ventas de la compañía.

Sin embargo, hay también aspectos negativos en esta expansión. Los márgenes en el sector del bourbon y del whisky son menores a los del vino. De forma general, en estos sectores hay mayor volumen pero menor fijación de precios. En caso de que no consigan el volumen necesario, el margen puede verse afectado por la dinámica de las economías de escala. Además, cada expansión le conlleva a TFF un periodo de flujos de caja disminuidos por la necesaria gran inversión inicial para adentrarse en un nuevo sector. Han demostrado habilidad para integrar y crecer sosteniblemente, pero este riesgo de ejecución me parece esencial tenerlo presente.

Como resumen, su modelo de negocio se basa en 5 pilares:

Crecimiento orgánico. Tanto el sector del vino como el sector de los licores tienen un crecimiento estructural que permite a la empresa disfrutar de un crecimiento orgánico moderado. Además, en épocas de menor demanda, los segmentos de diversificación y reparación de barricas permiten compensar la pérdida de la actividad en las barricas.

Integración vertical. Integración de todo el proceso productivo, desde la obtención de la madera hasta la venta de las barricas. Esto permite a TFF tener mayor conocimiento de los costes y disfrutar de mayores márgenes.

Sinergias. Las múltiples adquisiciones realizadas permiten a la empresa continuar su integración vertical y ahorrar costes por las sinergias. Este ahorre de coste no ocurre por centralizar las empresas, sino por poder compartir los recursos (como la madera).

Expansión horizontal. Tras consolidar su posición de líder en el sector del vino, la directiva decidió expandirse a otras bebidas con características comunes. Trasladaron su know how al whisky y al bourbon. Cabe la posibilidad de que en el futuro veamos expansiones a otras bebidas, como el cognac o el tequila.

Organización descentralizada. Las empresas que son adquiridas siguen operando de forma independiente. TFF Group es el paraguas que reúne a todas estas empresas, pero sin incidir en su actividad diaria. Esto favorece el espíritu emprendedor dentro del grupo.

Sector

La teoría prevaleciente sitúa el inicio del consumo del alcohol hace unos 9.000 años, con el surgimiento de la agricultura. Las primeras evidencias de la producción de alcohol son del 6000 a.C en Irán y Georgia. Con estos datos, podemos observar que el alcohol ha estado relacionado con el ser humano desde hace muchísimo tiempo. Desde su aparición, poco ha variado. Se han mejorado las técnicas de producción, conservación, distribución…pero las disrupciones han sido mínimas. El sector incluso ha superado periodos complicados, como el periodo de la ley seca en Estados Unidos. Esto nos refleja la resilencia del sector.

A continuación, veamos en mayor detalle los sectores a los que TFF atiende:

Vino

El mercado del vino es un sector maduro, con cientos de años de historia. Se estima que el mercado está valorado en 182 billones de dólares y va a crecer a un ritmo del 4% anual hasta 2028. El crecimiento del sector es menor a otras bebidas alcohólicas debido a que ya está muy bien establecida en nuestra sociedad. En países como España, Francia o Italia, el consumo de vino está muy extendido, por lo que el crecimiento vendrá dado por las personas que se conviertan en mayor de edad y una posible mayor penetración en países con menor consumo per cápita.

Como podemos observar en la gráfica anterior, el consumo mundial de vino ha decaído levemente en la última década, aumentando la cuota de mercado de otras bebidas alcohólicas. Sin embargo, a pesar de la caída de consumo, el precio medio de las exportaciones ha aumentado considerablemente. En mi opinión, esto puede reflejar que a pesar de la caída de la demanda a nivel total de unidades, cada vez hay mayor demanda de productos de mayor calidad y por lo tanto, de mayor precio.

Italia es el país con mayor producción de vino, situándose en 1200 millones de galones al año. Sus vinos son reconocidos internacionalmente por su calidad y denominación de origen. Francia sigue de cerca, situándose ligeramente por encima de los 1000 millones de galones anuales. Las uvas más famosas se sitúan en este país, como Cabernet Sauvignon, Chardonnay y Merlot. El tercer país con mayor producción es España, con aproximadamente 900 millones de galones/año. El clima español es ideal para la producción de vino, contando con productos muy famosos con denominación de origen como La Rioja o Jerez de la Frontera. Por último, Estados Unidos es un gran productor de vino, con 650 millones de galones al año. La mayoría de esta producción se produce en el estado de California, donde el clima es ideal.

En la última década, el mayor cambio que ha habido ha sido la forma de consumir el vino. Debido a la pandemia, las personas no pudieron acudir a los restaurantes y consumir el vino en estos establecimientos. En lugar de dejar de consumir vino, las personas empezaron a consumir más en sus domicilios. Esta tendencia continua a día de hoy, siendo el vino una bebida ampliamente popular en eventos sociales.

El principal riesgo del sector es su dependencia del clima para obtener una buena cosecha. La calidad del vino está relacionada con la calidad de la uva cosechada. El clima mediterráneo es ideal para la uva. Los inviernos suaves y los veranos cálidos y secos ayudan a la maduración óptima de la uva, permitiendo la concentración adecuada de azúcares y ácidos, que son esenciales para la calidad del fruto.

El riesgo de este sector viene de las consecuencias del cambio climático. El aumento de las temperaturas provoca que la maduración de la fruta no sea la óptima, además de una menor cantidad de precipitaciones. Si este riesgo se consuma, puede provocar que los tres países europeos con mayor nivel de producción (España, Italia y Francia) se vean gravemente afectados. Hay estudios que indican que debido al aumento de las temperaturas, la cosecha comienzan en promedio 13 días antes de lo que lo hacían antes de 1988. Es un riesgo latente a observar, pero que gracias a la diversificación de la directiva en otras bebidas, afecta en menor medida a la empresa.

Whisky

El mercado del whisky se estima que está valorado en 93 billones de dólares en 2024. Además, se espera que el mercado crezca un 3-4% anual hasta finales de la década actual.

A lo largo de este post me he centrado primordialmente en el whisky escocés, ya que es el sub sector del whisky donde TFF tiene mayor ventaja. Sin embargo, en la actualidad existen diversos tipos de whisky, todos caracterizados por su región de procedencia: irlandés, japonés, canadiense..

El crecimiento del whisky escocés ha sido menor al resto del mercado. La denominación de origen juega un papel fundalmental en limitar la oferta. Solamente se puede considerar whisky escocés si se cumple con una serie de condiciones, como madurar el producto por un mínimo de tres años en Escocia. Esto provoca que el crecimiento del sector en la última década haya sido de un ~2%.

Bourbon

El mercado de bourbon se estima que tiene un valor de 6 billones de dólares en 2022 y se espera que crezca un 6% anual hasta 2031. Es la bebida alcohólica con mayor crecimiento esperado dentro de los sectores que atiende TFF Group. A pesar de este alto crecimiento, el bourbon también limita su producción por motivos de denominación de origen. Para ser considerado bourbon, el producto debe contener con al menos 51% de maíz en su producción, reposar en barricas de roble blanco y ser producido en Kentucky.

Si nos fijamos en el crecimiento del sector hasta la actualidad, el crecimiento ha sido de un 5% CAGR. Es un crecimiento remarcable teniendo en cuenta el sector del que estamos hablando.

Si agrupamos tanto el whisky como el bourbon, el sector de los licores está teniendo un crecimiento superior al resto de sectores. La cuota de mercado de los licores respecto al resto de bebido aumenta cada año. El mercado de licores en Estados Unidos se estima que tiene un valor de 79 billones de dólares en 2024, y se espera que llegue e 101 billones en 2029, lo que supone un crecimiento del 5% anual.

Esto se debe a las siguientes tendencias:

Demanda creciente de productos premium. Cada vez hay un porcentaje mayor de población que se preocupa por la calidad de los alimentos que consume. Están dispuestos a pagar más por los productos a cambio de una mayor calidad. Esto favorece el consumo de los licores, con su proceso de maduración de calidad.

Cultura del cóctel. Los cocteles son concebidos como bebidas alcohólicas de mayor calidad. Son bebidas más caras por lo general, pero, la experiencia y la diversidad de los ingredientes atraen cada vez a mayor cantidad de personas. Para preparar estas bebidas, los licores son parte esencial.

Feminización y rejuvenecimiento de los consumidores. Ambos grupos sociales demandan cada vez más licores, por encima de cerveza ó vino, ya sea por tendencia social o por las dinámicas anteriormente expuestas.

Exploración de regiones. Se espera que licores no tan ampliamente consumidos actualmente, como el whisky canadiense o el japonés, aumenten sus ventas debido a la demanda de nuevas experiencias.

Diversificación de gamas. Distintas marcas están ampliando su oferta para acercar a los distintos tipos de cliente un perfil de licor adaptado a sus características.

El auge del sector del licor no solamente se refleja en la demanda de bebidas. Si observamos el número de destilerías artesanales en Estados Unidos, vemos un crecimiento explosivo. En 2005 se estima que había un centener de ellas, actualmente hay más de 2600. Además, se ha formado un turismo alrededor del sector del alcohol. Escapadas a museos, bodegas, destilerías, rutas..cada vez son más comunes entre la población adulta. Generalmente son perfiles de consumidores asiduos que se empiezan a interesar más por las experiencias alrededor de las bebidas alcohólicas.

Estados financieros

Desde 2015, los ingresos han crecido un 13% CAGR, llegando a 444M de euros en 2023. Ha habido años de crecimiento intenso, debido a crecimiento inorgánico o aumento de la demanda atrasada de años previos. Sin embargo, también ha habido años de apenas crecimiento y disminución en las ventas. Esto se debe al carácter industrial de la compañía, donde en ocasiones la demanda se postpone.

Si desglosamos por segmentos de producto, obtenemos el siguiente resultado:

Podemos observar como claramente el segmento del bourbon ha sido la línea de negocio con mayores crecimientos. Hay que tener en cuenta que gran parte de este crecimiento es inorgánico. El sector del vino ha crecido sus ingresos a un ritmo del 5,7% CAGR, el whisky al 4,4% CAGR y el bourbon al 62% CAGR.

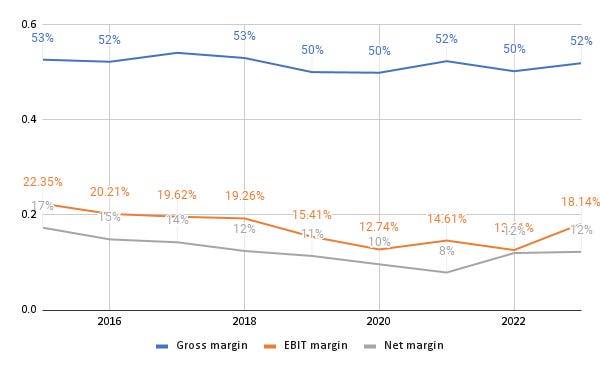

Respecto a los márgenes, el margen bruto ha oscilado entre el 50 y el 53%, mostrando resilencia en distintos momentos del ciclo. Son márgenes muy buenos, parecidos a alguna empresa tecnológica. Esto puede reflejar la calidad de su artesanía, que se traduce en mayores precios y márgenes. Sin embargo, debido a la gran integración vertical de la empresa, en periodos donde el crecimiento es menor, el margen operativo y el margen neto sufren. También hay que destacar el gran capex de crecimiento que TFF ha invertido en el sector del bourbon. En un periodo de normalización de este capex deberiamos ver mayores márgenes.

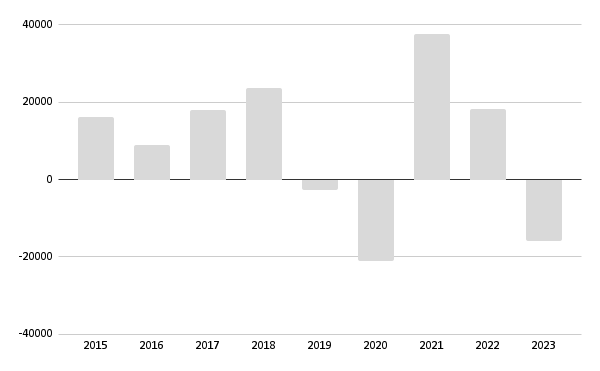

Respecto a la generación de caja, el ciclo de alto capex de crecimiento más periodos de un mayor gasto en working capital, ha provocado que haya años con flujos de caja negativos. Eso si, son sucesos esporádicos, ocurriendo en 2 de los últimos 9 años.

TFF Group es capaz de convertir, de media, el 61% de su resultado neto en flujo de caja. Si utilizamos las ventas totales como referencia, esta conversión baja hasta el 14%. Si observamos la evolución del flujo de caja libre, esta métrica se ha visto afectada en mayor medida por el ciclo de alto capex y mayores requerimientos de working capital. El FCF ha crecido, de media, un 16% y el FCF Margin (FCF/Ventas) se sitúa en el 4%.

Es importante tener en cuenta el altísimo nivel de capex de crecimiento desde que se inició la expansión al sector del bourbon. Alrededor de 400M de euros han sido destinados a construir la posición relevante de la empresa en el sector. Gracias a este gran desembolso, la empresa es capaz de producir 720.000 barriles anuales. La estrategia de la empresa es invertir 60M de euros adicionales para aumentar la capacidad hasta el millón de barriles anuales. Aparte de este capex, habrá que destinar recursos a cubrir necesidades adicionales de working capital.

Los niveles de deuda de la empresa son muy bajos. Al ser una empresa familiar, el interés de los propietarios es asegurar la supervivencia de la empresa a largo plazo. Por ello, incluso a pesar del gran ciclo de capex de crecimiento mencionado, la empresa ha mantenido siempre niveles de deuda bastante bajos. También, existe una partida en el balance registrada a coste histórico, stock de madera, valorada en 180M de euros. Sin embargo, el valor actual de ese stock es de prácticamente el doble.

En septiembre de 2023, TFF Group anunció una nueva adquisición, Biossent. Esta compañía fue creada en 1989 y está especializada en la trituración, calentamiento y extracción de roble para obtener extractos que pueden utilizarse en la producción de vinos y licores. A priori, se integrará en el segmentos de diversificación. Las ventas anuales de Biossent superan los 4 millones de euros y según el reporte de TFF Group, disfruta de una alta rentabilidad.

Además, el pasado enero la empresa anunció los resultados H1 23-24 (el año fiscal empieza en Junio en lugar de seguir el año natural). Los ingresos crecieron un 13,6% YoY. Si desglosamos este crecimiento, el sector del vino creció un 3,5% (4,7% LfL) y el sector de licores un 25% (31,1% Lfl). El sector vinícula se vió afectado por un mercado más relajado y problemas climáticos que afectaron la cosecha. Mientras tanto, el sector de los licores continuan su tendencia ascendente. Los precios del whisky subieron un 36%. Los ingresos del bourbon aumentaron un 21% gracias al aumento de ventas de barriles (tienen como objetivo fabricar 750.000 barriles anuales), aumento de precios y el aumento de la venta de madera (unidad de negocio de diversificación).

Los márgenes mejoraron en ambos segmentos debido al estricto control de costes y la mejora de márgenes del bourbon. Para este año preveen un capex de 38, millones, la mayoría es capex de crecimiento para el bourbon (no especifican cantidad exacta). Sin embargo, los inventarios aumentaron (debido al bourbon) y hubo un aumento del working capital para apoyar el crecimiento del negocio. Además, el aumento de las materias primas impactaron el working capital.

Directiva

TFF Group es una empresa familiar. Fundada por Joseph Francois en 1910, la famila Francois ha seguido administrando la empresa desde entonces. Actualmente, el CEO es Jerome Francois, siendo el bisnieto del fundador de la compañía. Es una persona muy importante en la historia de Tonnellerie Francois Frere debido a que él comienza la diversificación del negocio. Con Jerome, TFF empieza a mirar más allá del mercado vinícola.

Desde que asumió el cargo de CEO en 1989, Jerome Francois ha mejorado sustancialmente la posición competitiva de la empresa. A través de adquisiciones, ha colocado a TFF en una situación donde es capaz de superar a su competencia por know how y escala. Esto también le ha permitido tener visión acerca del rumbo a donde se dirige el sector de las bebidas alcohólicas. De ahí, las expansiones al whisky escocés y al bourbon.

Actualmente, la familia Francois posee el 70% de las acciones de la compañía, a través de distintos holdings y acciones a nombre personal. El porcentaje se ha mantenido estable, incluso ha aumentado con compras de acciones a nombre personal del CEO. Esto asegura que la directiva tiene soul in the game, siendo la supervivencia de la compañía su mayor foco.

La política de remuneración a la directiva es bastante simple, solamente reciben un salario fijo por parte de TFF. La remuneración total a la directiva fue de 3M de euros en 2023, representando un 0,67% de los ingresos totales. En este tipo de compañías, podríamos pensar el dividendo repartido a los accionistas como otra forma de remuneración, debido al porcentaje tan elevado de ownership. El dividendo repartido por TFF ha crecido desde 0.2 euros/acción en 2015 hasta el 0.6 euros/acción en 2023 (CAGR del ~22%). A pesar de las múltiples adquisiciones realizadas, no ha habido emisión de acciones. A continuación, os muestro una tabla con las empresas adquiridas desde 2016 (DISCLAIMER: no he incluido compras de fábricas y aserraderos; considero que se deberían concibir como capex en lugar de M&A):

Respecto a las guidances, suelen darlas mirando a 5 años vista. Son conscientes de que sus actividades están marcadas por vaivenes en el ciclo y preveen resultados para el final de cada ciclo. Además, suelen cumplirlas.

Sobre el capital allocation, el flujo de caja generado ha ido dirigido a financiar la expansión al sector del bourbon, necesidades de working capital y repartir dividendo. Más allá de observar los porcentajes, me parece relevante incidir en el motivo de la diversificación hacia los licores. Observaron un mercado muy maduro como es el sector del vino, con dependencias externas relevantes (el clima y las cosechas), y decidieron invertir fuertemente en construir su ventaja competitiva tanto en Whisky escocés como en el bourbon. Ambos licores comparten la característica de tener la oferta limitada por ser bebidas con denominación de origen, por lo que ser el primer jugador en adentrarse en este sector fue primordial. Tuvieron visión a largo plazo y lo hicieron, a pesar de pasar por un periodo de menores márgenes, menor generación de caja y mayor gasto. Veremos como se desarrollan los acontecimientos en el futuro, pero a priori, parece ser que tomaron la decisión correcta. Es un management con un conocimiento profundo del sector y totalmente alineados con los accionistas.

Ventajas competitivas

Know how. La fabricación y restauración de barricas necesita de un know how que solamente se puede obtener a través de la experiencia y de la cualificación de tus empleados. Es la ventaja competitiva más débil de TFF, puesto que teóricamente la competencia puede contratar a estos empleados. Sin embargo, todo el proceso de fabricación y revisión de la calidad es dificilmente replicable. Cualquier competidor tendría que imitar y mejorar la totalidad del proceso. Mejorar una sola parte del proceso no tendría impacto en TFF Group, puesto que el proceso en total tiene mayor valor que cada actividad por separado.

Economías de escala. La internacionalización y la diversificación del negocio ha aumentado esta ventaja competitiva. Es necesario invertir mucho dinero para crear toda la infraestructura necesaria para competir a TFF. Además, al actuar en mercados altamente regulados, el efecto de la ventaja de escala se multiplica. No hay mercado suficiente para más jugadores. Quizás puedan aparecer empresas que intenten robar cuota de mercado en algunos de los subsectores, pero parece improbable que un competidor pueda competir a TFF en la totalidad de sus operaciones. En el sector del alcohol, esta es la ventaja competitiva más importante. Por último, pienso que es relevante concebir esta ventaja competitiva no solamente como TFF Group es la empresa más grande, sino también concebir el tamaño relativo de la empresa dentro de cada sub segmento. Teniendo en cuenta la denominación de origen de las bebidas, TFF se tiene que situar rápidamente en la región geográfica correspondiente. Por ejemplo, para el bourbon, ha invertido decenas de cientos de millones para disponer de toda la infraestructura necesaria para obtener la ventaja de economías de escala en esta región. Al ser un mercado global pero de oferta limitada, la ventaja de mayor tamaño tiene más impacto. Si TFF ya tiene toda su red montada en Kentucky, esto quita incentivos a otras empresas de replicar su red.

Costes de cambio. Me parece la ventaja competitiva más importante de la empresa. Gracias a las características de las barricas de roble y su relevancia en el proceso de producción de las bebidas alcohólicas, los clientes que ya consumen los productos de TFF, encuentran poco atractiva la idea de cambiar de proveedor. En caso de que puedas ahorrar costes por cambiar hacia un competidor, este ahorro no compensa las consecuencias del cambio en el aroma y sabor de tu producto. Estos cambios en el producto podrían suponer la pérdida de tus clientes. Si comparamos esta posible consecuencia con el beneficio de ahorrar costes, el incentivo a cambiar de proveedor parece poco probable.

Riesgos

La empresa disfruta de múltiples ventajas competitivas sostenibles que es bastante probable que permitan a TFF mantener su posición competitiva en el sector. Sin embargo, una buena empresa no acarrea implícitamente que sea una buena inversión.

Desde la expansión al mercado del bourbon en 2015, TFF ha sufrido una disminución progresiva de los retornos sobre el capital invertido y un aumento del working capital necesario para continuar con la operativa habitual.

En primer lugar, es prudente esperar de este tipo de compañías con gran integración vertical con multitud de fábricas, inmobiliario…que tengan menores retornos sobre el capital invertido, debido a la gran base de capital utilizado para poder desarrollar su operativo.

Entiendo perfectamente que esto no es malo per se, la empresa ha preferido sacrificar el corto plazo por obtener ingresos del mercado de bebidas alcohólicas emergente de mayor crecimiento, lo cual es buena señal. Solamente es un pensamiento actual que me hace dudar de la empresa. Aún tengo trabajo por hacer en este aspecto para saber si este pensamiento es un sesgo que debería eliminar o simplemente es un filtro de calidad necesario.

En el gráfico de a continuación se puede observar cómo los retornos han disminuido progresivamente a medida que aumentaba el capex. También es cierto que a partir de que las inversiones realizadas han empezado a madurar, estos retornos han aumentado. Mi principal temor con esto es que ocurrirá cuando en lugar del bourbon, sea otra bebida alcohólica la que sea demandada. ¿Otro ciclo de 5 años de altísima inversión?

Por otro lado, el aspecto del working capital me genera aún más dudas. De media, entre 2015 y 2023, el NWC ha representado el 96% de las ventas. Es un negocio de altísima intensidad en capital. Repito, esto no es malo per se. Esto, de hecho, supone una barrera de entrada, puesto que hace falta mucho capital y know how para poder competir con TFF. Mis dudas van más dirigidas a la falta de oportunidades de invertir el capital más allá de financiar el working capital. Si combinas retornos al nivel de la media con poquísimo capital disponible para reinvertir, el resultado, en mi opinión, no es el más actractivo.

Tesis

Tras un periodo largo de gran inversión en capex de crecimiento y una mayor necesidad de working capital, la normalización de la inversión debería repercutir en una mayor generación de caja y conversión de efectivo por parte de la compañía. Para mí, este es mayor riesgo de la tesis.

El management está muy cualificado, posee grandes conocimientos acerca de su empresa, de su ventaja competitiva, del sector y de como debe TFF Group actuar en su sector. Poseen el 70% de las acciones en circulación y toman decisiones a largo plazo sin importar que a corto plazo suponga peores resultados en la visión de los mercados financieros. Esto es un punto muy positivo, que reduce bastante el riesgo de valor terminal.

En mi opinión, la tesis pasa por el repunte que puede tener la empresa una vez toda la inversión en el bourbon se normalice. La empresa debería ser capaz de crecer alrededor del 10% cada año sin mucha dificultad, entre crecimiento orgánico e inorgánico. También es cierto que es imprudente esperar que TFF Group vaya a crecer a doble dígito alto. Es una empresa resiliente, que crece sin parar pero sin prisa.

La empresa está muy posicionada en su sector y si es capaz de trasladar esta ventaja posicional en flujos de caja, es una empresa más que intersante.

Valoración

Para la valoración he construido un modelo muy simple con el menor número de suposiciones subjetivas posible. Los único inputs que he introducido ha sido un crecimiento anual del 10%, un aumento muy pequeño del margen neto y un múltiplo de salida de 15 veces beneficios.

Todas las suposiciones me parecen bastante conservadoras. La tasa de crecimiento de ingresos puede dar lugar a opcionalidad positiva, en caso de que el mercado de licores (whisky y bourbon) sigan disfrutando de demanda creciente. Además, con la integración vertical de la compañía, un 10% de crecimiento en ingresos debería trasladarse en un crecimiento mayor en el resultado neto. Este crecimiento más el dividendo, puede suponer una opción atractiva de rentabilidad.

Pienso que es bastante probable un aumento del margen neto a medida que se vaya integrando toda la capacidad adquirida por la expansión del bourbon. A corto plazo puede que no ocurra, debido al repunte de costes financieros por la subida de los tipos de interés y el stock acumulado de barricas, pero pienso que es posible a largo plazo.También debería haber un repunte del flujo de caja cuando el capex de crecimiento y el working capital se normalicen.

El múltiplo de salida de 15x beneficios me parece acorde. Es cierto que la calidad del negocio es mayor que la media del mercado: ventajas competitivas, sector estable, empresa familiar, directiva con soul in the game, visibilidad de retornos..etc. Sin embargo, hasta que la empresa no muestre que puede generar caja positiva de forma sostenida pienso que no es conservador en pensar sobre un múltiplo mayor.

El CEO de la compañía, en una entrevista, afirmó que para el ejercicio presente proyectaban unos ingresos aproximados de ~485 millones de euros, con márgenes operativos del más del 19% (extensión de márgenes vs FY2023). Si utilizamos esta guidance como proxy, obtenemos que la empresa está cotizando a aproximadamente 10x EBIT y 15x beneficios (precio de 42 euros/acción cuando escribo esto). Por último, en la misma entrevista, se afirma que TFF habría sido contactado por un grupo de capital privado que buscaba la compra del segmento de bourbon. El valor de su oferta era equiparable a la capitalización de la compañía, insinuando la infravaloración de la empresa.

Conclusión

TFF Group es una empresa familiar gestionada con mentalidad a largo plazo, forma parte de un sector que es bastante complicado que haya una disrupción y cuenta con varias ventajas competitivas sostenibles.

Tras haberla analizado, pienso que es una buena empresa, pero que no llega a ser excepcional. El riesgo a la baja me parece muy limitado, pero también me lo parece el upside. La generación de caja es muy dependiente de como administren el working capital, aspecto que no me entusiasma. Existen empresas con necesidades de capex y activos, pero con menor dependencia del working capital. Por ejemplo, en el caso de los retailers ó supermercados, estas empresas también necesitan una gran cantidad de activos, pero cuentan (generalmente) con working capital negativo. Esta dinámica provoca que la conversión de efectivo y la generación de caja sea más fácil. De momento, seguiré la compañía de cerca en espera de tener mayor visibilidad de su futuro. En caso de ver normalización de capex y generación de caja, mi interés aumentará considerablemente.

Otro pensamiento que tengo es sobre el coste de oportunidad. La empresa ha pasado por dos periodos que durante 5-7 años la acción no ha hecho nada. Sé que esta afirmación quizás entra en conflicto con decir que soy inversor a largo plazo, ya que lo que importa es el rendimiento del negocio y no de la acción. Sin embargo, pienso que el coste de oportunidad es relevante. Hay empresas industriales/cíclicas con periodos similares y son grandísimas inversiones, pero actualmente no sé si sería capaz de aguantar 7 años sabiendo el coste de oportunidad latente.

A la hora de invertir, busco generalmente dos tipos de empresas. En primer lugar, las empresas que considero que son excelentes y tengo la certeza de que pueden seguir creando valor a largo plazo (Hermes por ejemplo). Por otro lado, me interesan empresas que, por distintos motivos, pienso que pueden mejorar y alcanzar el estatus de muy buena empresa ó empresa excelente (The Italian Sea Group). Busco estos dos tipos de inversiones porque pienso que son las dos opciones que ofrecen mejores rendimientos ajustados al riesgo.

Por los motivos mencionados, pienso que TFF Group no es una empresa extraordinaria, bajo mi criterio. En caso de que opinéis distinto, os animo a comentar vuestras ideas. Estoy siempre dispuesto a debatir mis ideas con cualquier inversor.

No todo es negativo, gracias al estudio de la empresa he podido aprender de un sector resiliente, con catalizadores de crecimiento y sin riesgo a disrupciones, como es el sector de las bebidas alcohólicas. Pienso que es un muy buen sector para inversores a largo plazo. Empresas como Diageo han entrado a la lista de seguimiento gracias a esta tesis.

Disclaimer

Este artículo no es ni pretende ser una recomendación de compra y/o venta. Cada persona debe hacer su propia investigación antes de tomar una decisión de inversión.

Good summary. One thing to note on the high working capital is that it's mostly highest-quality oak being dried/aged before processing. This means book value of NWC is materially understated if they were to liquidate their wood supply as these will become more valuable over time.

Gracias por la tesis. en abierto Empresa que cómo dices a largo plazo puede ir bien (esta un el PER más bajo de los últimos años), pero con mucho working Capital, y mucho CAPEX. NO me gusta